BY LAURA ZILLMAN

One trillion dollars is a lot of money. To put it into perspective, one trillion dollars would pay the average salaries of all 535 members of Congress for ten thousand years.

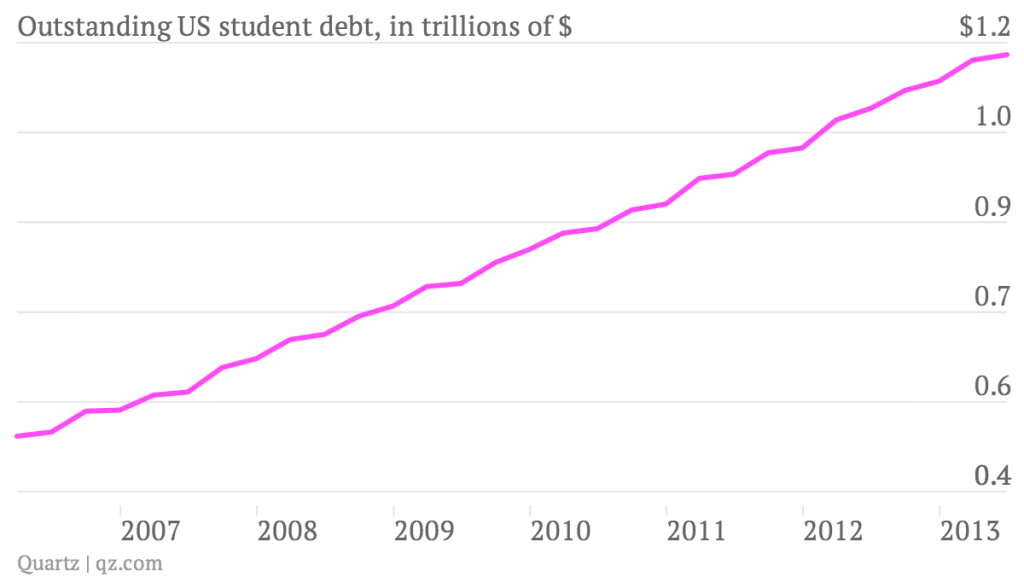

One trillion dollars is also a sobering number: the amount of student debt in the United States at the end of 2011. The average American college student graduates with $27,000 in debt—and the average GW student with more than $32,000. These numbers are nowhere in the minds of most freshly-minted college freshmen, who gladly sign loan agreements without a second thought.

The problem? That’s exactly what student loan lenders are counting on.

Adjusted for inflation, the average sticker price for tuition, room and board, and fees at private universities has increased 3.9% per year since 2002, but recent evidence finds that much of college spending has focused on non-academic purposes. Colleges now compete in an increasingly-cutthroat environment, luring students with luxurious dorms, amenities, and other perks.

Students who believe that they are getting their money’s worth will pay the price—and for what they don’t have, they will take out loans and expect to pay them back after graduation. They are never told that one in ten graduates will default on their loans, or that that defaulting could prevent them from buying a house, car, or starting a business one day. Declaring bankruptcy is not an option for most student loans, and horror stories of student debt ruining once-optimistic students’ lives are becoming all too common.

In a world where college degrees are deemed essential, and virtually any eighteen-year-old can borrow ever-larger sums of money to pay for ever-ballooning college costs, it is appalling that most of the time we don’t even know what we’re paying for. And far too often, we don’t get to participate in discussions of how our tuition dollars are spent.

It’s tough to argue that education is a social good when it’s used to ensnare our students, who are, quite literally, paying dearly for it.

One trillion dollars is also a sobering number: the amount of student debt in the United States at the end of 2011. The average American college student graduates with $27,000 in debt—and the average GW student with more than $32,000. These numbers are nowhere in the minds of most freshly-minted college freshmen, who gladly sign loan agreements without a second thought.

The problem? That’s exactly what student loan lenders are counting on.

Adjusted for inflation, the average sticker price for tuition, room and board, and fees at private universities has increased 3.9% per year since 2002, but recent evidence finds that much of college spending has focused on non-academic purposes. Colleges now compete in an increasingly-cutthroat environment, luring students with luxurious dorms, amenities, and other perks.

Students who believe that they are getting their money’s worth will pay the price—and for what they don’t have, they will take out loans and expect to pay them back after graduation. They are never told that one in ten graduates will default on their loans, or that that defaulting could prevent them from buying a house, car, or starting a business one day. Declaring bankruptcy is not an option for most student loans, and horror stories of student debt ruining once-optimistic students’ lives are becoming all too common.

In a world where college degrees are deemed essential, and virtually any eighteen-year-old can borrow ever-larger sums of money to pay for ever-ballooning college costs, it is appalling that most of the time we don’t even know what we’re paying for. And far too often, we don’t get to participate in discussions of how our tuition dollars are spent.

It’s tough to argue that education is a social good when it’s used to ensnare our students, who are, quite literally, paying dearly for it.

RSS Feed

RSS Feed